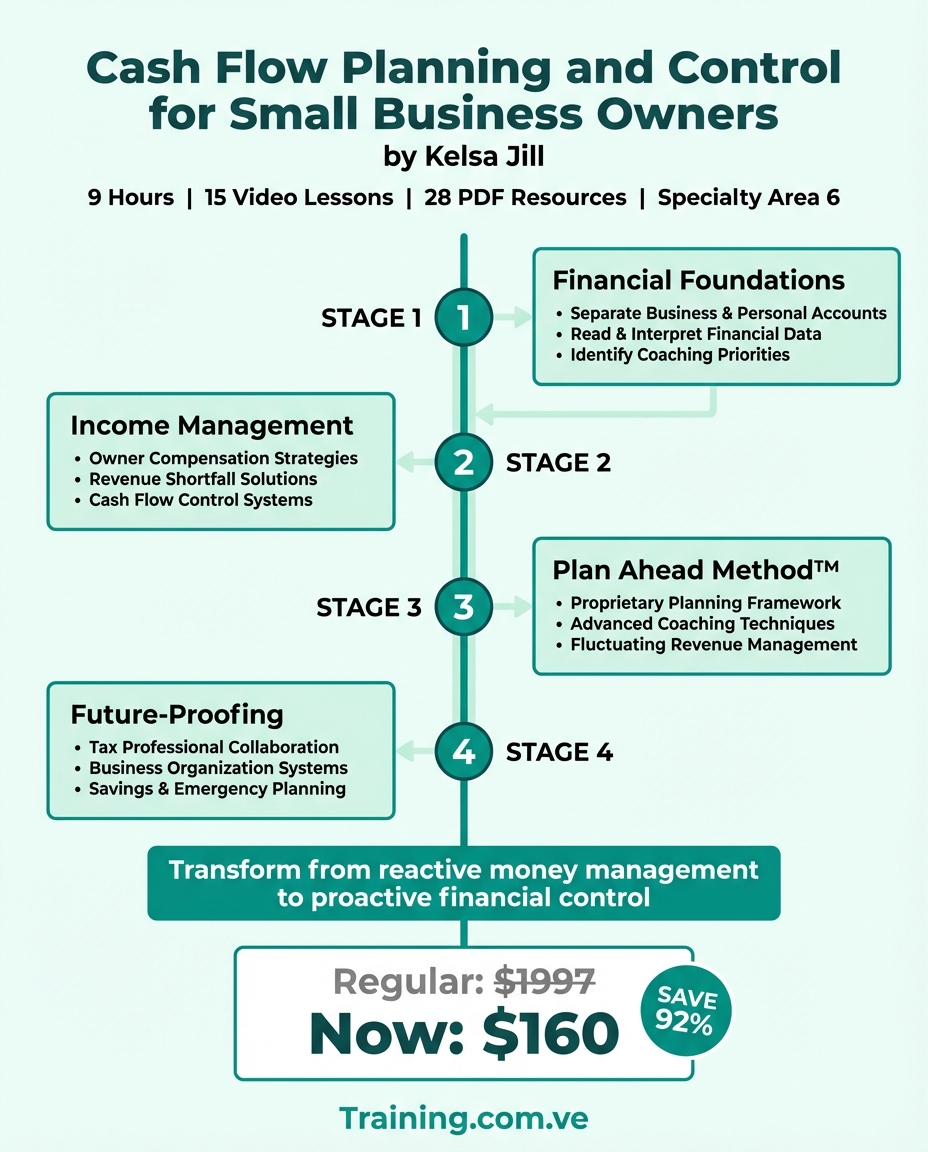

The Plan Ahead Method™ Explained: Forward-Looking Cash Flow That Shows Shortfalls Weeks Out — from Cash Flow Planning and Control for Small Business Owners by Kelsa Dickey

The Plan Ahead Method™ is Kelsa Dickey's rolling, forward-looking cash flow system from Cash Flow Planning and Control for Small Business Owners ($1,997, 15 lessons). It is the central framework of the course and the tool that distinguishes Kelsa Dickey's approach from standard backward-looking business budgeting. The core mechanism: revenue sits at the top of each column in a Google Sheets spreadsheet, expenses are listed below, and the ending balance automatically becomes the starting balance for the next period — giving business owners a live projection of cash position weeks before a shortfall arrives.

Most small business owners discover a cash flow problem the same way: the bank account runs lower than expected and a payment is due tomorrow. The response is reactive — a scramble to move money, delay an invoice, draw from savings, or make a phone call that feels embarrassing. The problem did not appear overnight. It was building for weeks. The owner simply had no system that showed it coming.

Kelsa Dickey, CEO and Money Coach at Fiscal Fitness Phoenix, built her career on a different premise: that cash flow problems are almost always visible in advance, provided the business has a system that looks forward instead of backward. The Plan Ahead Method™ is that system, and it sits at the center of her course, Cash Flow Planning and Control for Small Business Owners.

Who Kelsa Dickey Is

Kelsa Dickey's path to financial coaching is not the story of someone who always had money figured out. It is the story of someone who watched her mother file for bankruptcy in middle school, carried that experience through school as a question — what would it take to actually help people with their money? — and spent years in the wrong version of the answer before finding the right one.

She graduated with a bachelor's degree in Personal Finance, a minor in Economics, and later earned a master's degree in Accounting. She became fully licensed as a financial advisor — Series 7, Series 66, health, life, and disability insurance. She spent seven years as a financial advisor and corporate accountant. She was qualified, credentialed, and miserable, because the work was about making corporations more profitable rather than helping real people navigate real financial pressure.

Her last day in corporate America was March 25, 2008. She launched Fiscal Fitness PHX in 2010, built her practice around the clients traditional financial advising had never prioritized — individuals, couples, and small business owners who needed to understand their money at the level of the checking account, not the portfolio — and developed the Plan Ahead Method™ as the practical engine of that work.

The method is now used by thousands of people. Fiscal Fitness has facilitated over a million dollars in total debt elimination and helped clients accumulate hundreds of thousands in savings. The 15-lesson Cash Flow Planning and Control course, priced at $1,997, is the most concentrated delivery of the method as it applies to business finances.

The Problem the Plan Ahead Method™ Is Built to Solve

Traditional budgeting for small businesses tends to do one of two things: it tracks where money went after it left the account, or it produces an annual projection that sits in a spreadsheet and is never updated.

Both of these approaches are backward-looking in practice. They tell you what happened. They do not show you what is about to happen.

The result is a business owner who is perpetually surprised. Revenue came in, expenses went out, and somewhere in the gap between those two things, a shortfall appeared. The owner knows, after the fact, that payroll was tight in October or that November's vendor payments had to be juggled. But they do not know in September that October is going to be tight — and that is the only time they could have done something about it.

The core insight is this: cash flow management is not an accounting problem. It is a visibility problem. The numbers are knowable in advance. The issue is that most business owners do not have a system that organizes those numbers in a way that reveals the future instead of documenting the past.

What the Plan Ahead Method™ Is

The Plan Ahead Method™ is Kelsa Dickey's rolling, forward-looking cash flow system built in Google Sheets. Its architecture is deliberately simple: revenue at the top of each column, expenses listed below revenue, and an ending balance that automatically becomes the starting balance for the next column.

Each column represents a period — a week, a bi-weekly pay cycle, or a month, depending on the layout variation the business owner chooses. The ending balance at the right edge of each period does not disappear. It flows directly into the left edge of the next. This single mechanical feature — the rolling balance — is what transforms a budget from a historical record into a forward-looking instrument.

When the system is populated with anticipated revenue (invoices due, recurring contracts, expected deposits) and known expenses (payroll, rent, subscriptions, loan payments, quarterly tax estimates), the owner can see, four to eight weeks in advance, what their ending balance will look like at the end of each period. If a period ends with a negative balance or a balance that falls below a minimum threshold the owner has set, that shortfall is visible before it becomes a crisis.

What makes this different from a standard monthly budget is the advance notice built into the architecture. A cash flow shortfall identified six weeks out is a planning problem. The same shortfall identified three days out is an emergency. The Plan Ahead Method™ is designed to keep business owners operating in planning mode rather than emergency mode.

Get Every Framework from Cash Flow Planning and Control for Small Business Owners

The course costs $1997. All frameworks extracted — $49/year.

Start free — 10 full summaries, no credit card

The Five Layout Variations

One of the differentiating features of the Plan Ahead Method™ as taught in the course is that it is not presented as a single rigid template. Kelsa Dickey teaches five distinct layout configurations, each suited to a different business structure or cash flow pattern.

Simple Bi-Weekly LayoutThe foundational version. Columns represent two-week periods, matching a standard bi-weekly payroll cycle. Revenue lands at the top of each bi-weekly column; expenses are mapped to the period in which they are due; the ending balance rolls forward. This layout works well for service businesses with predictable bi-weekly billing or payroll obligations and gives owners a four-to-twelve-week forward view depending on how many columns they build out.

Weekly with X-MarkingA higher-resolution version of the same rolling structure, with one additional layer: a simple X-marking system to distinguish between revenue and expenses that have been confirmed versus those that are anticipated. When an invoice is paid, it gets marked. When an expense clears, it gets marked. This allows the owner to see, at any point in the week, which items in their plan have materialized and which are still projected — a meaningful distinction in businesses where revenue timing is variable.

Deposit Account LayoutThis variation separates the cash flow view by account, with a dedicated column structure for the deposit account distinct from the operating account. It is particularly useful for businesses that receive large deposits or retainers in advance of delivering services, where there is a real and important distinction between money that has been received and money that has been earned. The layout makes that distinction visible in the sheet and prevents owners from spending deposit-account funds as if they were operating-account funds.

Operating and Fixed SplitThis layout divides expenses into two categories within each period: fixed obligations (rent, loan payments, insurance, subscriptions with set monthly amounts) and operating expenses (variable costs, team hours, supplies, discretionary spending). The visual separation makes it immediately apparent how much of each period's revenue is already spoken for before any variable spending occurs. This is particularly useful for business owners who are trying to understand their true break-even threshold or identify where discretionary cuts are actually available.

Credit Card IntegrationThe most structurally complex of the five layouts, this variation incorporates credit card charges and payment cycles into the rolling balance. Expenses charged to a business credit card do not hit the bank account when they are incurred — they hit when the card payment clears. The Credit Card Integration layout accounts for this timing gap explicitly, mapping card charges to the period in which they are incurred for planning purposes while also showing the bank account impact in the period when the payment posts. This prevents the common situation where an owner sees a healthy bank balance without accounting for the credit card statement that is about to come due.

This is one of 7 frameworks in Cash Flow Planning and Control. The complete breakdown — including the Plan Ahead Method templates, Deposit Account setup, and Compensation Progression stages — is on Course To Action. Free account, 10 summaries, no credit card. Or unlock all 110+ courses for $49/30 days.

Why the Rolling Balance Is the Core Mechanism

Of all the structural choices in the Plan Ahead Method™, the rolling balance is the one that changes how owners actually think about their cash position.

A static monthly budget shows you a forecast for each month in isolation. If January projects a $12,000 surplus and February projects a $4,000 deficit, those are two separate pictures. The rolling balance system shows you that February starts with January's surplus — meaning February's apparent deficit is actually a net positive, or that the surplus needs to be preserved rather than spent in order to cover February's gap.

This changes the decisions an owner makes in January. With a static budget, January looks fine and February looks like a future problem. With a rolling balance, January's decisions are immediately visible as inputs into February's starting position. The month-to-month connection becomes part of how the owner reads the sheet, and that changes how they authorize spending, time revenue collection, and plan for irregular expenses.

The forward-looking nature of the system also changes the owner's relationship to revenue collection. When the sheet shows that the next period starts with a shortfall unless a particular invoice is collected before a specific date, chasing that invoice stops feeling like administrative nuisance and starts feeling like a direct response to a known problem. The system makes the stakes of each financial action legible in a way that a static budget or a bank balance does not.

In summary, the rolling balance is not a cosmetic change to spreadsheet layout — it is a structural change to what the spreadsheet is actually for, shifting it from a historical record to a forward-looking operational instrument.

What This Framework Does Not Cover

The main limitation of the Plan Ahead Method™ is scope: it is a cash flow visibility system, not a pricing model, a revenue growth strategy, or a tax optimization tool. It will show you that your cash position is deteriorating in three weeks — it will not tell you whether to raise your prices, restructure your service packages, or bring on a new revenue stream to close the gap. Those are decisions the business owner still has to make; the system gives them the information to make those decisions with more lead time.

The method also works best when revenue is at least partially predictable. Businesses with extremely lumpy or irregular income — project-based agencies, seasonal businesses with sharp peaks and valleys, businesses transitioning between models — will find the system harder to populate accurately. Kelsa Dickey addresses this within the course, including approaches for planning under revenue uncertainty, but the system is inherently more powerful when revenue timing is known or estimable.

The Framework in Context

Cash Flow Planning and Control for Small Business Owners is a 15-lesson course structured to move a business owner from a reactive relationship with their bank account to a forward-looking system that shows shortfalls weeks before they arrive. The Plan Ahead Method™ is the framework that makes that possible.

This is best suited for service-based business owners under $1M in revenue who have been running their finances on feel — one account, irregular pay, no forward projection — and financial coaches who need a deployable methodology to offer business owner clients.

For business owners who have tried standard monthly budgets, annual projections, or simply monitoring their bank balance and found all of those approaches insufficient — insufficient being the word for "I keep getting surprised" — the architectural difference in the Plan Ahead Method™ is worth understanding. The rolling balance is not a cosmetic change. It is a structural change to what the spreadsheet is actually for.

The course costs $1,997. Before you spend that, read the full breakdown of all 7 frameworks on Course To Action — free account, 10 summaries, no credit card required. Every summary includes audio. The "Apply to My Business" AI tool has read the entire course and can generate a custom cash flow plan for your specific situation. Or unlock all 110+ premium courses for $49/30 days — one payment, no auto-renewal.

Not a review. Not a rating. A complete framework-level analysis so you know exactly what you're buying — or whether you need to buy it at all — before you spend $1,997.

Course To Action publishes independent framework-level breakdowns of online courses — the 20% that delivers 80% of the value, so you can make an informed decision before you spend a dollar.Get All Frameworks from Cash Flow Planning and Control for Small Business Owners

The course costs $1997. The complete breakdown is $49/year — every course on the platform.

This is one framework. Course To Action has every framework, every lesson, and AI that applies it to your specific business. Read or listen — every summary has audio.

Start free — 10 full summaries, no credit card required